E Choice Updates

September 2019

Recession Housing Price Discussion Overlaps Rate Hold

Despite predictions of cuts in the coming months, the RBA has decided to leave the official cash rate on hold for September. At the same time, many economists are frantic at the prospect of a looming recession. With the US and China locked in a trade war, waning post-GFC growth and our already low cash rate, many are worried about Australia’s ability to fare in the current economic outlook. Join us as we discuss the impact this could have on our housing market, including our past and current ability to cope. HINT: it’s not all dire straits.

The word ‘recession’ strikes fear into the hearts of anyone who hears it mentioned. So, when economists start discussing if the rebound in housing prices is going to be short-lived due to a looming recession, naturally the ears of homeowners within hearing distance prick-up.

Now while the word recession sounds formidable, the fact that housing prices are star ting

to recover from a slump, and that the Reserve Bank of Australia has once again left rates on hold are both favourable.

ting

to recover from a slump, and that the Reserve Bank of Australia has once again left rates on hold are both favourable.

Why?

Well, let’s take an in-depth look at what’s occurred recently, and in the past, so we can put your mind at ease about recession and it’s impact on housing prices.

Recession Housing Price Discussions

Economists are talking about a recession. Now for those of you who don’t know what a recession is, it is defined as two fiscal quarters (six consecutive months) where economic growth declines.

Looking at the global economy, economists have noticed that markers are pointing toward the U.S. entering into a recession. This outcome is linked to trade wars between China and the U.S. and also post-GFC growth waning.

Many economists will argue, however that the U.S. has been in recession before – 2000 and 2008 – and Australia has managed to dodge any repercussions. Other economists, though, highlight that back then Australia had more resilience – our deficit wasn’t as high or our cash rate as low – and this gave us more ‘wriggle room’ if the economy looked like taking a nosedive.

Other factors that economists remind us of occurred back in 2000 and 2008. Back then, we didn’t have such high household debt, or non-existent wage growth, as we do now.

But the stabilisation of the housing market in established and new dwellings is looking promising. According to Tim Reardon, the Housing Industry Association (HIA) chief economist, the stabilisation of housing prices will continue, providing that the credit squeeze subsides and the industry meets, rather than exceeds demand.

Australia’s Last Recession and the Recession Housing Price

The last time Australia experienced a recession was in the 1990s. At the same time, recession housing prices were flat, and in some areas, prices were dropping.

However, not all markets weakened during the 1900s recession – Melbourne recorded price drops of over 6%, but Queensland stayed steady – which is similar to what occurred in the latest housing market decline where Sydney and Melbourne's prices plummet, and Tasmanian property defied the downturn.

The way that the housing market will respond to a recession, therefore, depends on the type of recession. For instance, if it’s financial, then recession housing prices in Sydney and Melbourne are likely to be hardest hit. If, however, the recession is resource-related, then Western Australia is the most likely to suffer.

Historical Housing Price Changes During Economic Downturn

Looking back at historical housing data during the 1990s recession and the Global Financial Crisis, which occurred in 2008, it becomes apparent that while some housing markets became volatile, not all reacted the same way to economic changes. Some markets showed little or no signs of change during an economic downturn due to their state, city or town economy keeping them buoyant.

But historical data also shows that all Australian states and territories have experienced recession multiple times since the mid-80s. For example, Sydney faced nine months of declining gross domestic product (GDP) during the 2012-13 financial year, which technically means the city was in recession. And yet, between 2013-2017 the same city realised a 70% increase in property prices.

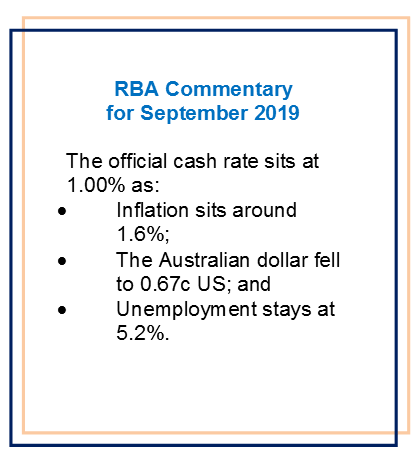

During the 1990s recession, the national GDP dropped by 1.7%, and unemployment in Australia rose from 7.4% to 10.1%. In comparison, during the first quarter of 2019, the Australian GDP rose by 2%, and unemployment hovered around 5.2%. Although many larger companies such as Big W, owned by Woolworths Limited, are closing stores that are not performing, which could increase Australian unemployment levels.

With the 1990s recession came housing price declines in some capitals, while other capitals realised growth. Sydney and Melbourne's home values declined by 7% and 2.3% respectively, whereas Brisbane property prices increased by 6.8% and Hobart dwelling values rose 4.3%.

If we compare the 2008 GFC, 2014 Mining Downturn and the 2018 Credit Crunch, then the impact on different markets becomes more apparent.

| Changes in Dwelling Values During Economic Shock |

.jpg)

|

|||

| All Dwellings % | ||||

| City or Region | GFC 2008 | Mining Downturn 2014 | Credit Crunch 2018 | |

| Sydney | -6.2 | 18.4 | -9.9 | |

| Melbourne | -8.3 | 23.5 | -8.2 | |

| Brisbane | -4.7 | 7.2 | -2.4 | |

| Adelaide | -3.1 | 10.3 | -0.8 | |

| Perth | -6.8 | -20.0 | -8.9 | |

| Hobart | -3.5 | 35.9 | 2.8 | |

| Darwin | -2.1 | -29.3 | -8.7 | |

| Canberra | -3.2 | 22.3 | 1.1 | |

| Combined Capitals | -6.1 | 13.2 | -7.3 | |

|

Source: CoreLogic |

||||

The 2008 GFC differed to the 1990s recession. All capital city markets witnessed a drop in home values, though some were far less than others. The period of decline for Australia proved relatively short after the GFC, and the market recovered quickly.

Whereas the mining downturn in 2014, only effected Perth and Darwin housing markets. Sydney, Melbourne, Hobart and Canberra markets prospered because they weren’t reliant on mining resources.

The recent Credit Crunch, where lending criteria tightened, was a different story. This change restricted investor lending nationwide and made it harder to borrow, so it affected a higher proportion of the market. As a result, most Australian markets declined in value.

All of these economic shocks highlight how different types of economic change impact on the housing market. Plus, they showcase how the housing market adapts to these changes and recovers. Therefore, it becomes apparent that no matter the financial ripple, the housing market is quick to rebound.

Are you looking for a more competitive mortgage? If you said YES, then don't hesitate to get in touch.

Arrange Your FREE

No-Obligation Meeting

Either phone us on (02) 9791 1779 or complete the form below

Download now and get your

business off to a flying start!